Corporate surveys in November show that the pace of growth is still accelerating in the Euro Area. This can be seen at the global level but also in every sector, notably in the manufacturing sector where the stronger momentum is consistent with a higher international trade dynamics. Surveys also show that employment is increasing rapidly and that nominal pressures remain limited.

This environment doesn’t give clue on the way the ECB monetary policy will be manage in the future. Inside the European Monetary Authority we perceive at least three ways of thinking on the future of monetary policy.

The main trend is that the inflation rate will not accelerate even in the current context of rapid growth. Therefore the ECB could continue to purchase assets after September 2018 (Draghi, Praet)

Some think that the recovery will rapidly lead to higher inflation (its trend will be perceived as consistent with the ECB target) The purchases could stop in September (Coeuré)

The last trend is to stop purchases at the end of the year.

Surveys cannot help to choose between the first and the second trend. Growth is following a stronger momentum than expected but the inflation rate and inflation expectations remains low. We continue to follow Draghi.

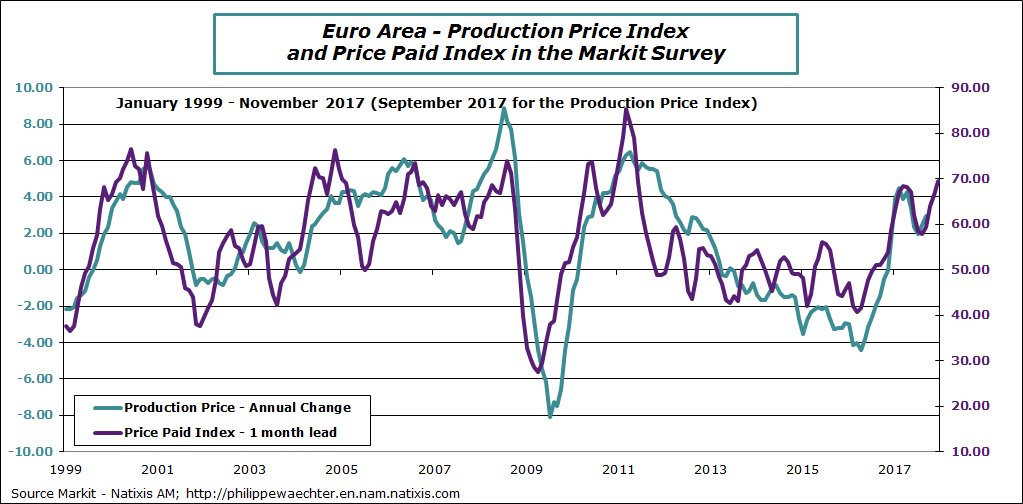

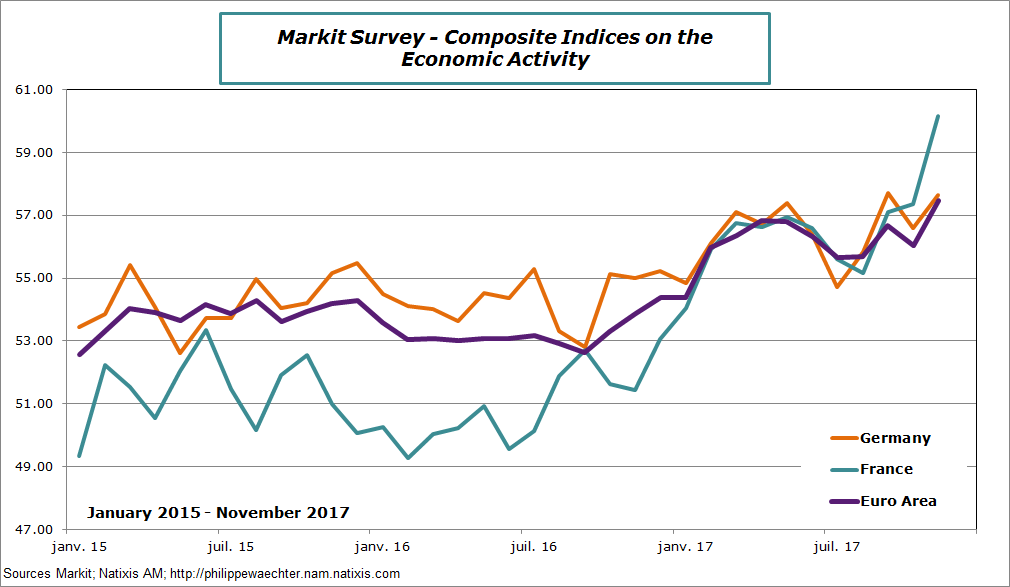

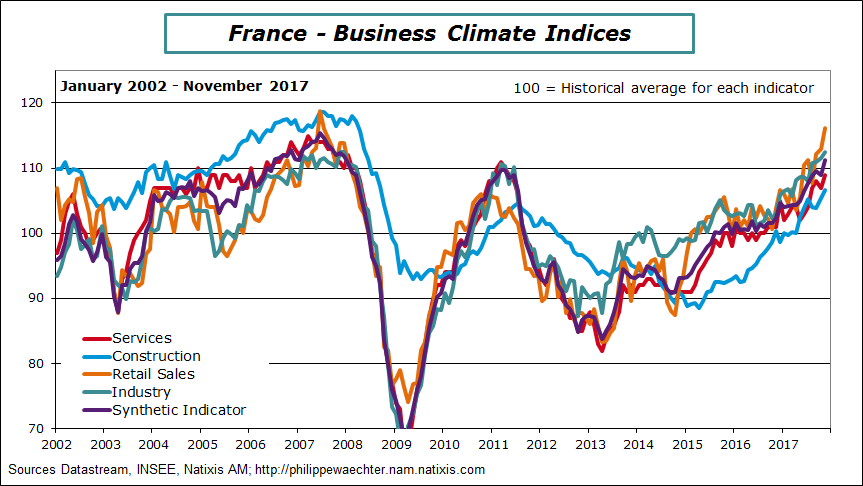

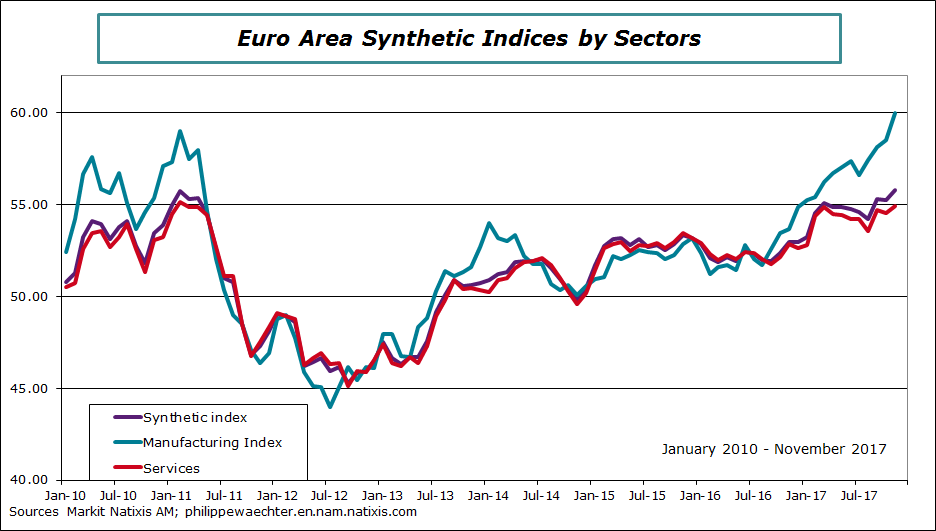

5 graphs can illustrate this boom in the economic activity

Graph 1 – Synthetic indices are on the upside and France is leading the European economy. The catching up process for France can be seen after the end of 2016. It is impressive.

Graph 2 – In France, all the economic sectors have a strong momentum. Construction is accelerating rapidly. This balanced dynamics suggests that the growth process is here for long

Graph 3 – The growth momentum in the manufacturing sector is impressive. This reflects a stronger trade dynamics and shows that the rest of the world continues to grow rapidly.

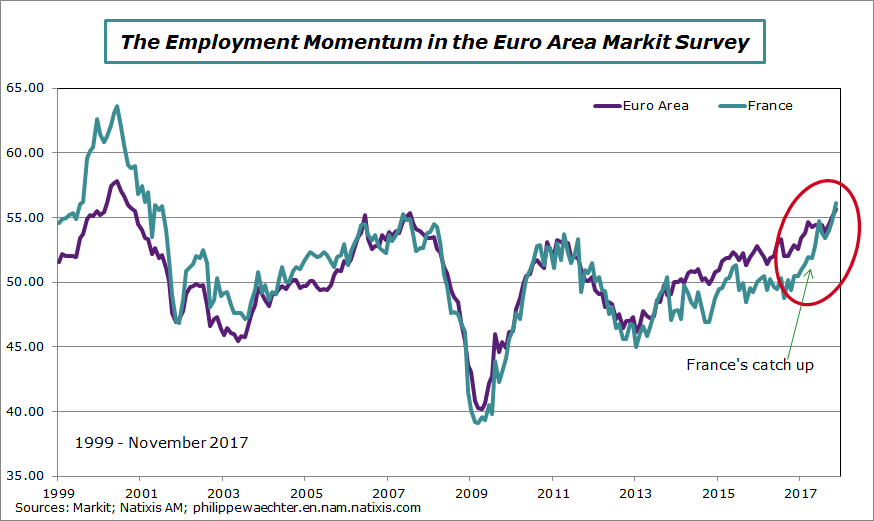

Graph 4 – The employment level is at its highest since the beginning of the 2000’s leading to a virtuous and self sustained growth. The domestic demand is the main engine for growth.

Graph 5 – Nominal pressures remain limited. This doesn’t tell us something on the future of the inflation rate and on the way the ECB will react.