The European Central Bank is meeting today. In her press conference, Christine Lagarde will clarify the ECB’s position on the crisis stemming from the conflict in Iran. She will also provide indications of what monetary policy might be pursued in the coming months.

One important point to note, however: the forecasts presented will have been established before the start of the conflict. The June projections will therefore be more relevant.

The central bank’s attitude towards an inflationary risk, such as that brought about by rising energy prices, will depend on its trade-off between activity and inflation.

We have become accustomed to thinking in terms of activity, assuming that inflation would never be a long-term phenomenon. This corresponds to the period of great moderation.

Since the mid-1980s, due to controlled inflation and strong mechanisms to bring it back to a low level even in the event of a shock, central banks have aligned their reaction with economic activity.

In the event of a spike in oil prices, the shock was perceived as temporarily inflationary and therefore not persistent. Consequently, the central bank’s actions should focus on economic activity and assume that the impact of energy prices would not create a lasting imbalance.

Since the shock was temporary, it was necessary not to create, by increasing interest rates, conditions that would cause a risk of a lasting downward inflection in activity.

However, there have been other situations in which inflation has been persistent.

During the first oil shock but also from the summer of 2022 when the price of gas soared in Europe.

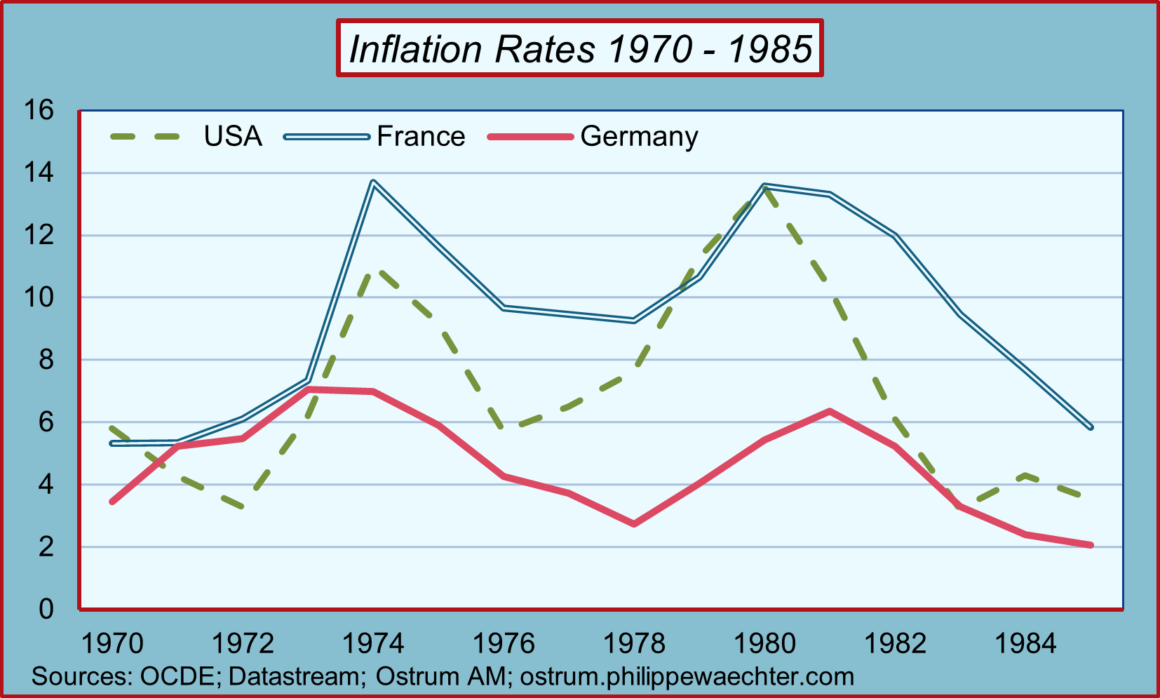

The illuminating point here is the behavior of the Bundesbank in the 1970s.

Before the first oil shock, it had begun to tighten its monetary policy. Economic activity was then growing rapidly, creating strain on the productive apparatus.

The oil shock, in which prices quadrupled permanently, fostered the idea that inflation could be persistent. The Bundesbank then traded inflation for economic activity. The message was to prevent inflation from rising, even if it negatively impacted economic activity. The Bundesbank adopted a restrictive policy.

France, the United Kingdom and the United States then had a more accommodative strategy of cushioning the oil shock in order not to penalize demand and activity.

As a result, German inflation was moderate. From the last quarter of 1972 to the last quarter of 1983, the inflation rate in Germany averaged 4.9% annually, compared to 8.2% in the US, 10.9% in France and 13.1% in the United Kingdom.

The question posed today is that of the risk of persistent inflation due to sustained tensions on energy prices.

Should the central banks’ arbitrage be the same as that seen during the Great Moderation when inflation systematically fell below the ECB’s target?

Or has the world changed, with the risk of inflation becoming entrenched because the oil shock has a lasting effect? In one case, the ECB does nothing; in the other, it must tighten monetary conditions.

Given the uncertainties surrounding the Strait of Hormuz, option 2 is not indefensible. This option 2 no longer appears to be completely discredited.