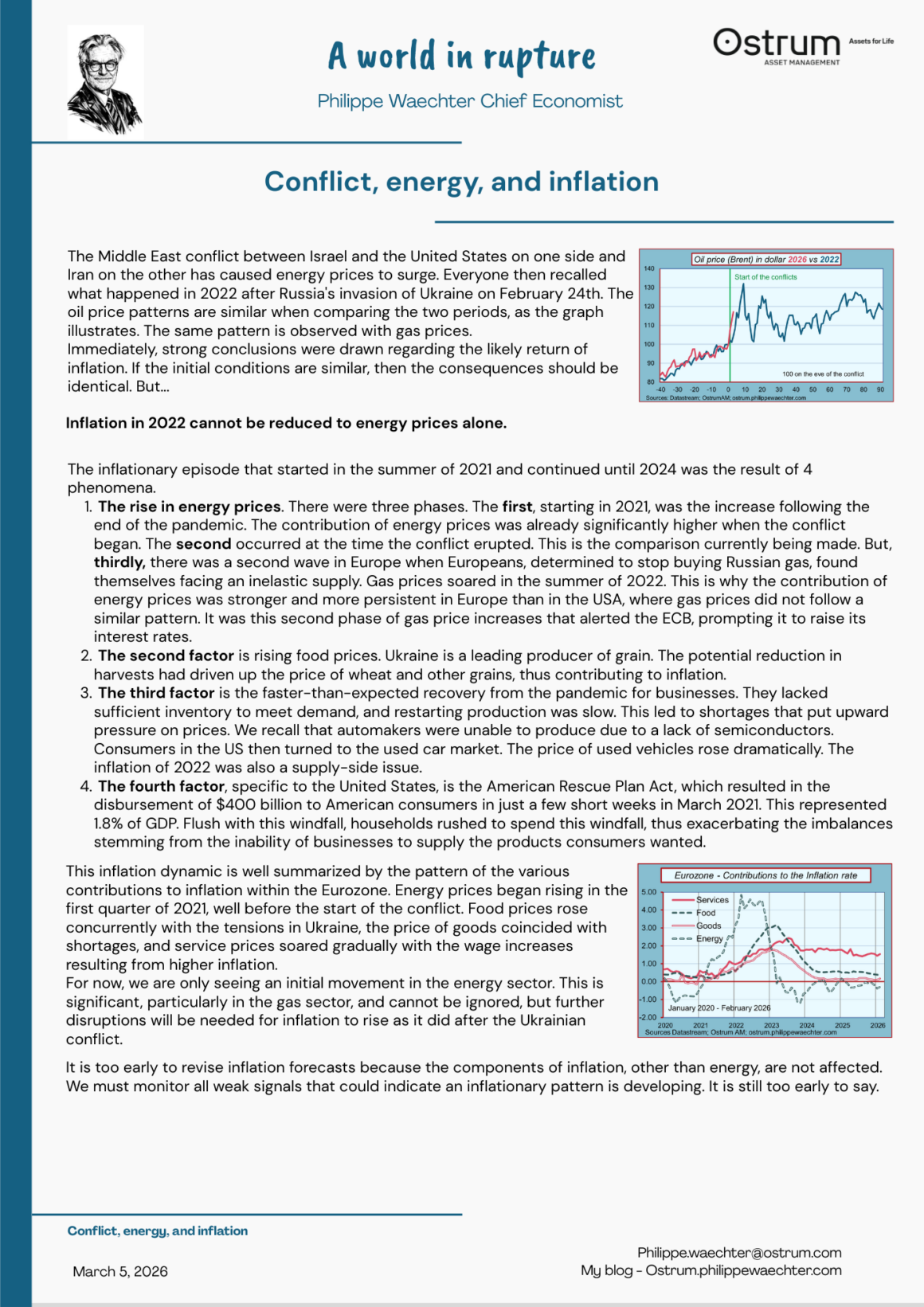

The Middle East conflict between Israel and the United States on one side and Iran on the other has caused energy prices to surge. Everyone then recalled what happened in 2022 after Russia’s invasion of Ukraine on February 24th. The oil price patterns are similar when comparing the two periods, as the graph illustrates. The same pattern is observed with gas prices.

Immediately, strong conclusions were drawn regarding the likely return of inflation. If the initial conditions are similar, then the consequences should be identical. But…

Inflation in 2022 cannot be reduced to energy prices alone.

The inflationary episode that started in the summer of 2021 and continued until 2024 was the result of 4 phenomena.

The rise in energy prices. There were three phases. The first, starting in 2021, was the increase following the end of the pandemic. The contribution of energy prices was already significantly higher when the conflict began. The second occurred at the time the conflict erupted. This is the comparison currently being made. But, thirdly, there was a second wave in Europe when Europeans, determined to stop buying Russian gas, found themselves facing an inelastic supply. Gas prices soared in the summer of 2022. This is why the contribution of energy prices was stronger and more persistent in Europe than in the USA, where gas prices did not follow a similar pattern. It was this second phase of gas price increases that alerted the ECB, prompting it to raise its interest rates.

The second factor is rising food prices. Ukraine is a leading producer of grain. The potential reduction in harvests had driven up the price of wheat and other grains, thus contributing to inflation.

The third factor is the faster-than-expected recovery from the pandemic for businesses. They lacked sufficient inventory to meet demand, and restarting production was slow. This led to shortages that put upward pressure on prices. We recall that automakers were unable to produce due to a lack of semiconductors. Consumers in the US then turned to the used car market. The price of used vehicles rose dramatically. The inflation of 2022 was also a supply-side issue.

The fourth factor, specific to the United States, is the American Rescue Plan Act, which resulted in the disbursement of $400 billion to American consumers in just a few short weeks in March 2021. This represented 1.8% of GDP. Flush with this windfall, households rushed to spend this windfall, thus exacerbating the imbalances stemming from the inability of businesses to supply the products consumers wanted.

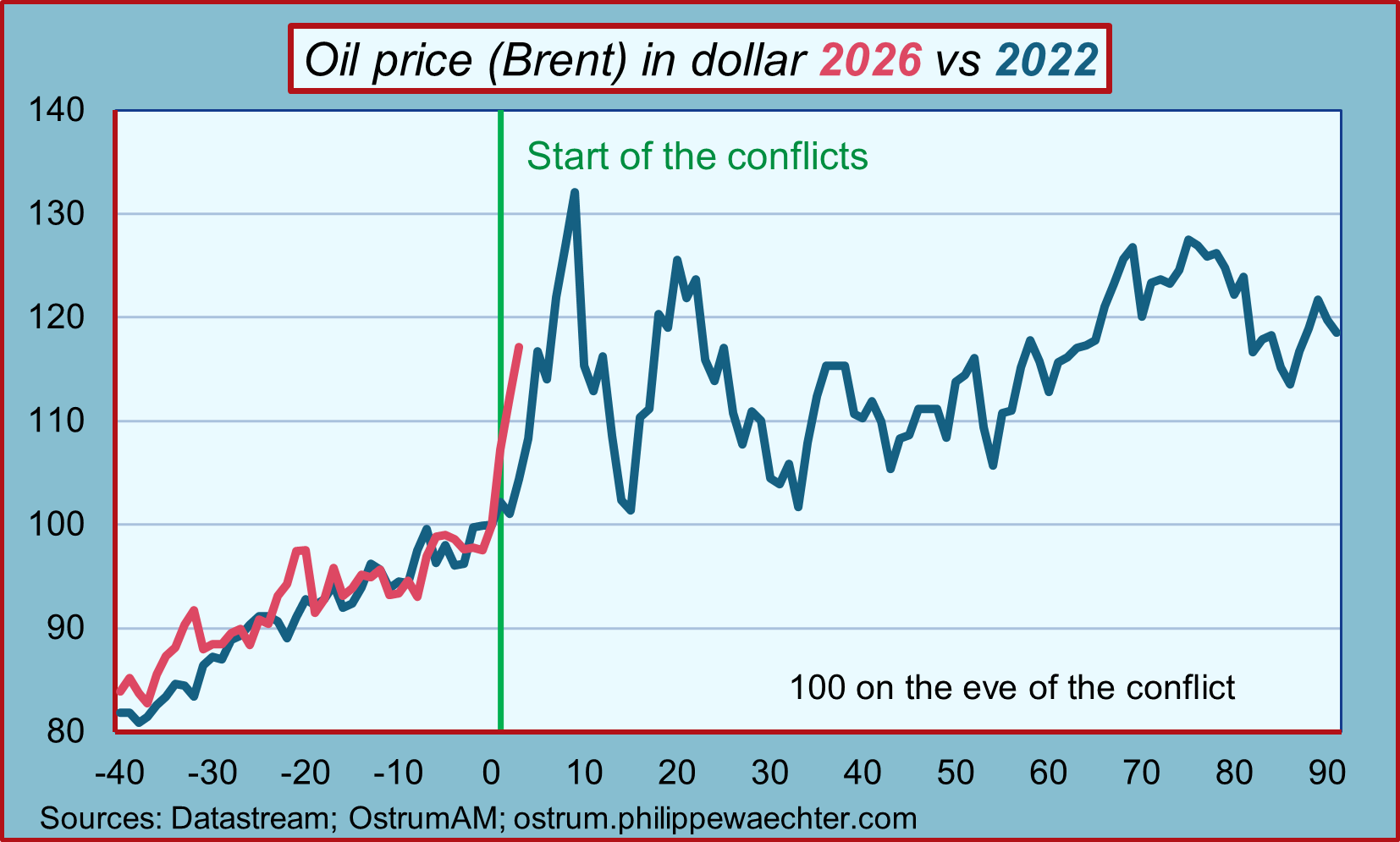

This inflation dynamic is well summarized by the pattern of the various contributions to inflation within the Eurozone. Energy prices began rising in the first quarter of 2021, well before the start of the conflict. Food prices rose concurrently with the tensions in Ukraine, the price of goods coincided with shortages, and service prices soared gradually with the wage increases resulting from higher inflation.

For now, we are only seeing an initial movement in the energy sector. This is significant, particularly in the gas sector, and cannot be ignored, but further disruptions will be needed for inflation to rise as it did after the Ukrainian conflict.

It is too early to revise inflation forecasts because the components of inflation, other than energy, are not affected. We must monitor all weak signals that could indicate an inflationary pattern is developing. It is still too early to say.