Developed countries’ economies were enjoying robust growth in the first half of 2008, despite some initial cracks that had been appearing since the previous summer. That was ten years ago, and since then, world economic dynamics have transformed completely, as the sources of momentum and adjustment systems have changed, especially in developed countries.

We could potentially identify a whole raft of differences but I have focused on six that I feel are useful in helping us understand the new world economic order.

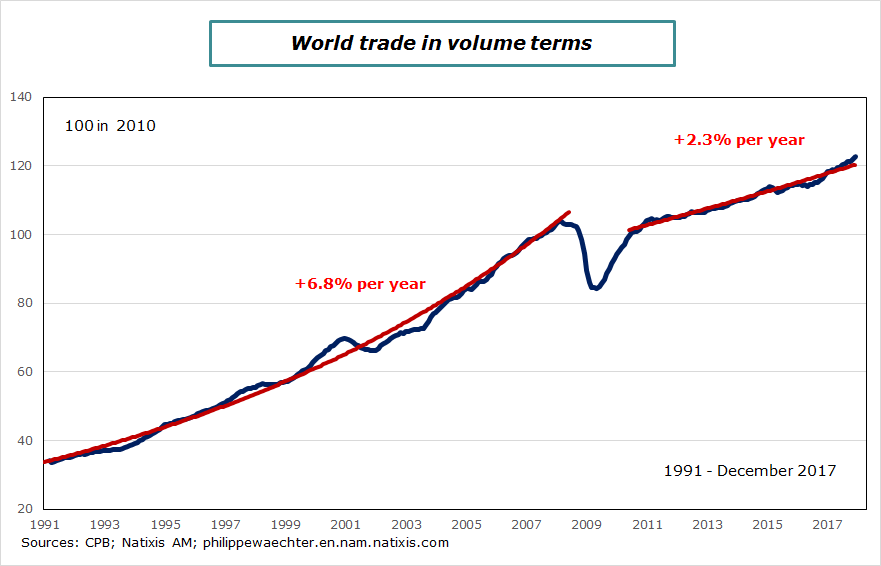

1 – World trade is no longer growing at the same pace

World trade has entirely changed pace since the crisis in 2008. Before that date, it fluctuated fairly broadly around a trend estimated at 6.8% per year in volume terms, thereby creating a strong source of momentum in each economy and driving economic growth, with an overall virtuous dynamic between trade and economic activity.

But since 2011, world trade has seen little fluctuation and the trend is now at 2.3%. The turning point in 2011 can be attributed to austerity policies and in particular programs implemented in Europe. So momentum that can be expected across the rest of the world is no longer on a par with past showings. This change is significant for Europe as the continent used to wait for the rest of the world to pick up a pace before staging its own improvement, and this explains the systematic time lag in the cycle between the US, which traditionally recovered very sharply after a negative shock, and Europe, which always seemed to be lagging slightly.

A weaker trend, more sluggish world growth and also a different way of working for world trade. Developed countries make a less significant contribution because they display weaker industrial momentum and this configuration means that fresh sources need to be found to spark off some renewed economic activity momentum.

The impetus created by start-ups in France is useful in this respect if it creates a new economic landscape via the development of new companies beyond this first level.

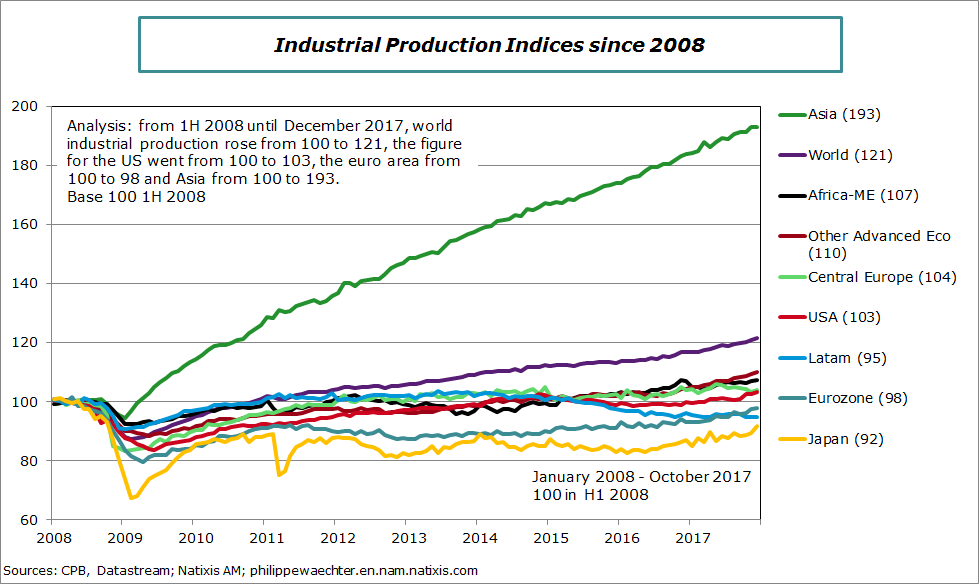

2 – The world balance has changed

If we are to get a clearer grasp on world momentum and the reasons behind sluggish world trade, it is vital to realize that over the past ten years, developed countries have no longer been making a positive contribution to world industrial activity growth, which is at the very heart of world trade, but Asia has taken on this role stunningly.

The chart below shows that world production gained 21% between 2008 and end-2017, but gains were only 3% in the US vs. 93% in Asia excluding Japan.

This shift in manufacturing momentum suggests that the source of economic growth that can lead to productivity gains and therefore provide a strong and long-term competitive advantage is now located in Asia, and no longer in either Europe or the US.

In France, this situation leads to a focus on sectors that cannot be sold out. The French government has just defined its strategic sectors, reflecting a defensive attitude to a fast-changing world where we latch onto aspects that look vital for the long term.

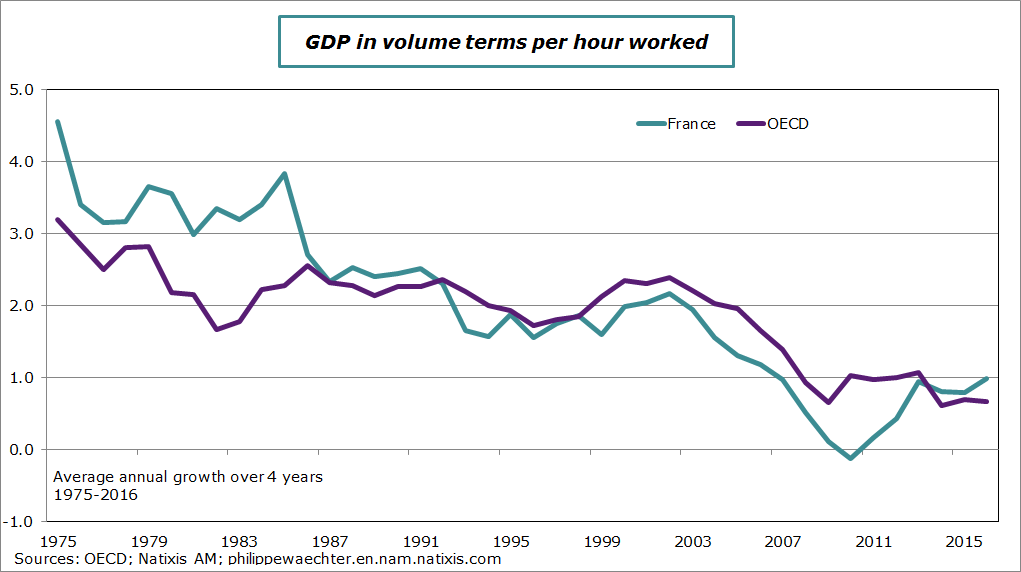

3 – Slowdown in productivity gains

Since the start of the crisis and despite ever-increasing innovation, we are seeing a slowdown in productivity gains in industrialized countries, with a clear downturn for France and all G7 countries on the chart.

Western economies are no longer able to generate the surplus that is required to pay out higher incomes and also finance the social security system. The downtrend in working hours and the rise in incomes drove western economies to generate a high surplus, but this is no longer the case. It is now much more difficult to make significant strides forward in social progress e.g. how do we calculate the transfer from the working younger generation to the retired older generation to fund pensions, when young people’s income is no longer rising as quickly due to low productivity gains? What incentives can be provided to encourage the younger generation to keep on working hard?.

The decline in productivity reflects the consequences of sluggish demand resulting from the financial crisis on the one hand, and the temporary increase in productivity witnessed at the end of the 1990s on the other. These phenomena also combined with the remarkable transformation sparked by the digitalization of the economy, which leads to extensive adjustments and adjustment costs.

The challenge is to suggest that these first two negative factors will only be temporary and that the impact of innovations will be positive and may even increase in the long term, yet we have no visibility on the timeframe for this momentum to take root, as western economies have become increasingly diverse, particularly as companies do not have the same ability – or desire – to digitalize. And so we see vast differences between companies, even for companies within the same sector, which will take a long time to disappear. It is vital to take all possible measures to support these adjustments, and public spending has a key role to play in this respect.

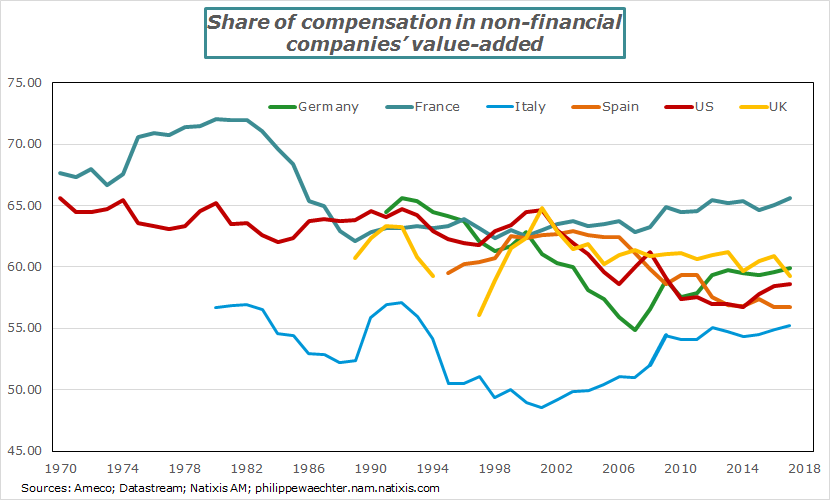

4 – Sharing of value-added has become more advantageous for companies

The sharing of value-added has shifted to the advantage of companies, particularly since the financial crisis, and the weighting of wages in value-added has declined in most developed countries.

This also reflects and shows lower employee bargaining power and goes part way to explaining the lack of wage inflation. This situation is further amplified by lower trade union participation.

A good illustration of this point is the change in wage-setting in the US. I recently noted that the share of one-time bonuses was increasing to the detriment of salary increases, thereby avoiding the permanent and recurring impact of salary increases on companies’ cost structures. This lack of salary increases allowed for implementation of unconventional monetary policies.

So some new light has been cast on one of the questions on economic adjustment. The inability to boost wages when unemployment is falling quickly is a new adjustment model that does not involve a strong and swift restriction on the cycle to regulate it and avoid permanent imbalances. So monetary policy can now be accommodative in the long term.

France is swimming against the tide somewhat in this respect. The share of wage costs has increased significantly over recent years, or in other words, corporate margins have narrowed since 2008. The macroeconomic adjustment after the fall of Lehman Brothers mainly took place to the detriment of companies. The French Competiveness and Employment Tax Credit and the Stability Pact merely served to push this indicator back to the zone it was in previously. This means that we shouldn’t expect any great things from these programs, but rather we are simply getting back to the pre-crisis balance and French companies have not gained any major advantages compared to others.

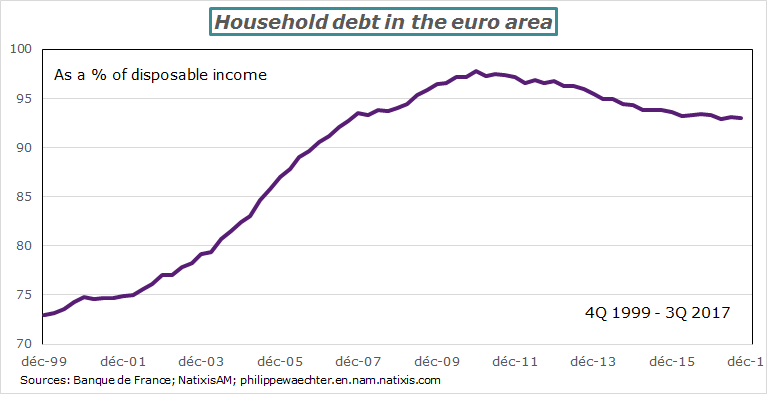

5 – Household debt remains high

The financial crisis was triggered by rising household debt, especially on mortgage loans. When we look at the euro area, we see that this type of debt has not really decreased in the past ten years: looking at Banque de France data, this figure increased considerably from 73% of available income when the euro area was set up, to 97.8% in 2010, while in the third quarter of 2017, the figure stood at 93%, slightly below the 2010 high. However, this figure does not provide strong leverage for additional debt as was the case during the first part of the 2000s decade. Productivity gains are lower, so we cannot expect strong income growth, and this trend can potentially drive the secular stagnation scenario. The consumer spending profile will therefore continue to hinge on payroll trends i.e. the number of jobs multiplied by wages. Wages are not rising much, so job momentum will therefore be crucial, and this is the rationale we are witnessing in the UK: there are a lot of jobs but they are badly paid. This is not good news, especially in the UK where this situation still allowed households to take on even more debt. Any surge in domestic demand momentum will most certainly be capped by this continued excessive debt level.

6 – Global political balance is no longer naturally cooperative

Before the financial crisis, the political balance was seen as being fairly cooperative: each country had a role to play in the worldwide context, and each felt that it had something to gain from this cooperation.

The recent shift in economic momentum as I mentioned above as regards industrial production changed this perception. The lowest earners in developed countries felt like workers in emerging countries, where growth is now much more robust than in the developed world, were catching them up. Donald Trump’s arrival to the White House and the Brexit vote in the UK showed that a different balance to the pre-crisis situation was possible. The US has become unpredictable and is gradually moving away from Europe, while the UK is chasing a dream. However, we can see the knock-on effect of this situation, especially in Poland and a number of countries across central Europe. Meanwhile, China is also standing out with its “Belt and Road” program, as it aims to set up a trade framework and network to serve its own interests.

It is vital that this situation sets the stage for the euro area and Europe to recover more influence in the new political order, but as the French prime minister Edouard Philippe recently stated, this involves agreeing on a common strategic culture…yet this type of strategy cannot be cooperative.

There has been a whole slew of changes in the past ten year. The world economy no longer derives the same impetus from either world trade or productivity gains. Meanwhile, the deterioration in wage bargaining power no longer leads to nominal shifts allowing the implementation of long-term accommodative monetary policies to offset these changes. This implies that the normalization of monetary policy with no accompanying improvement in fundamentals (trade and productivity) will not be the ultimate solution to mark a return to normal. Inadequate productivity gains are the real problem for western economies as they cannot claw back leeway in managing the economy, and this is the real issue that economies will need to tackle. Innovation momentum should help but it remains just an important criterion if there is no real joint effort to embark on this quest.