The collapse of industrial production foreshadows what the future figures could be in the Euro zone.

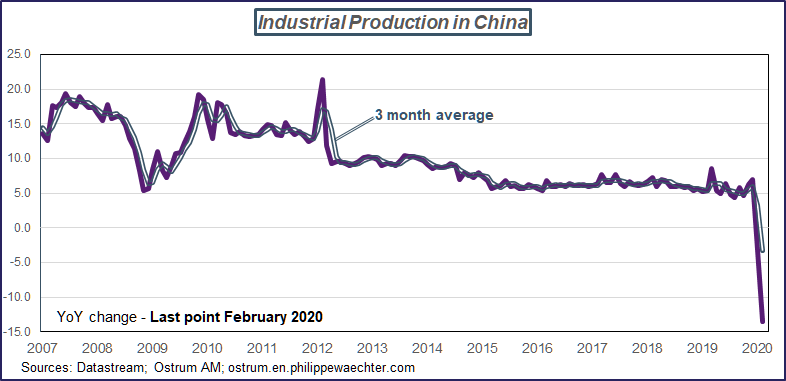

The collapse of Chinese industrial production is spectacular. The figures were expected to decline after February’s surveys. Over one year, in February, production fell by -13.5%.

In 2008/2009 during the financial crisis, it had not decreased. It had slowed down to 5% growth over a year.

The February figure shows a break and suggests the extent of the Chinese slowdown in the first quarter.

It is also a measure of the impact the epidemic could have. The shutdown of the Italian economy, that of Spain since this weekend and to a certain extent that of France (pending complete containment) must be gauged by one of these Chinese data.

To imagine that the growth of the euro zone could be maintained close 0% (even if by daring we put a small negative sign in front of it) is rubbish. Collective immunity, which is the path chosen by Germany, rather than confinement, simply risks prolonging the inflection of the euro zone since the German brake will come late.