According to companies’ survey in Germany and in France the economic activity was marginally down in August. German’s companies were a little more pessimistic for the 6 month period to come.

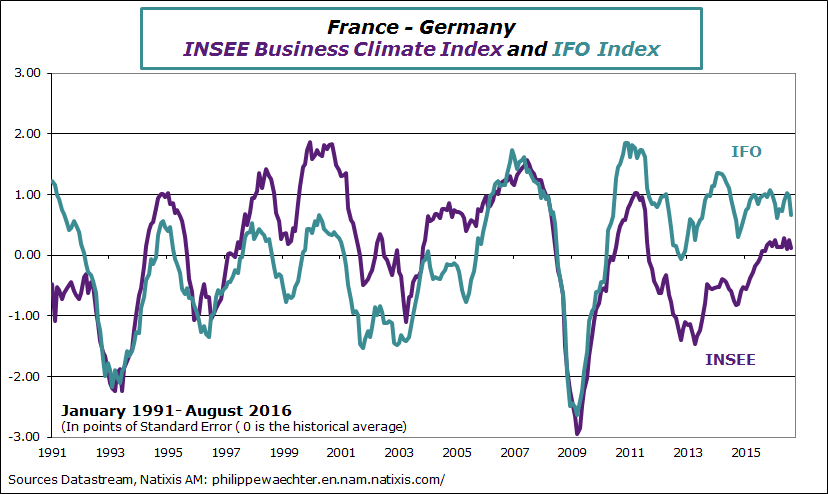

Even if levels are different we perceive in the following graph that there is a kind of stability in economic activity during the last twelve months. This synchronization of the business cycle suggest that France and Germany cannot really expect a stronger growth momentum in the short run. In other words, it seems that German and French economic activity are not able to accelerate from their current level. It’s not worrisome for Germany as its unemployment rate is low but it is problematic for France as its unemployment rate is just below 10%. As there is no impulse from outside as world trade trend is flat, it means that the impulse must come from inside. The ECB has done the job so we must expect a more proactive fiscal policy in order to jump on a higher trajectory.

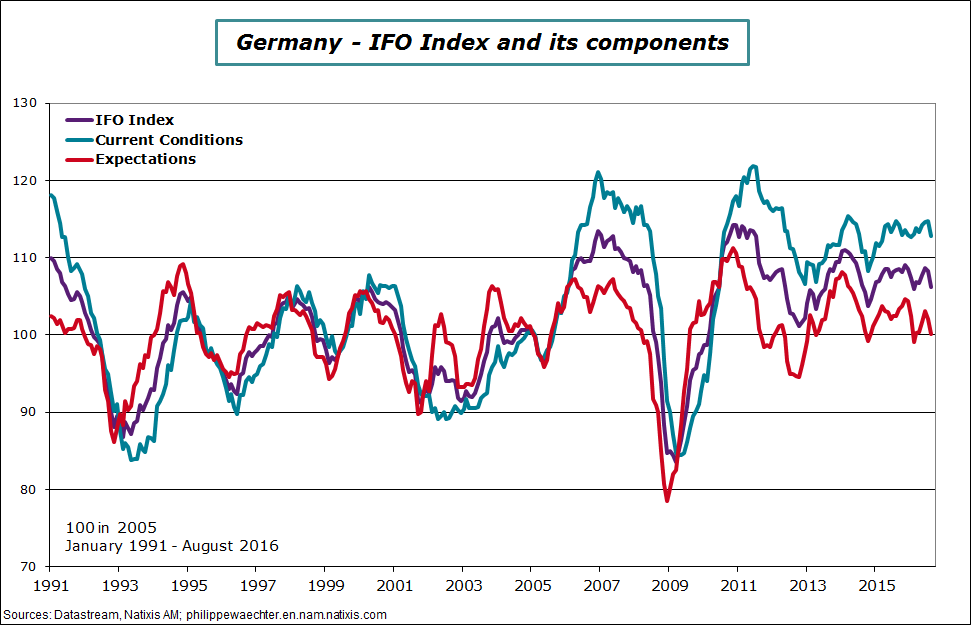

For Germany, the main source of weakness is a slowdown in expectations. The index is back to 100.1 which is marginally below its historical average (100.3). The current condition index (112.8) is weaker but at a level way above its historical average (103.2)

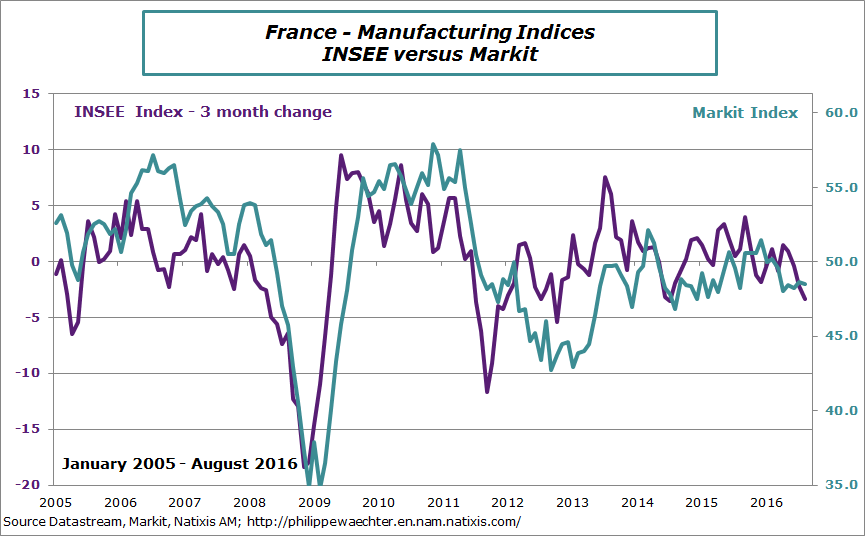

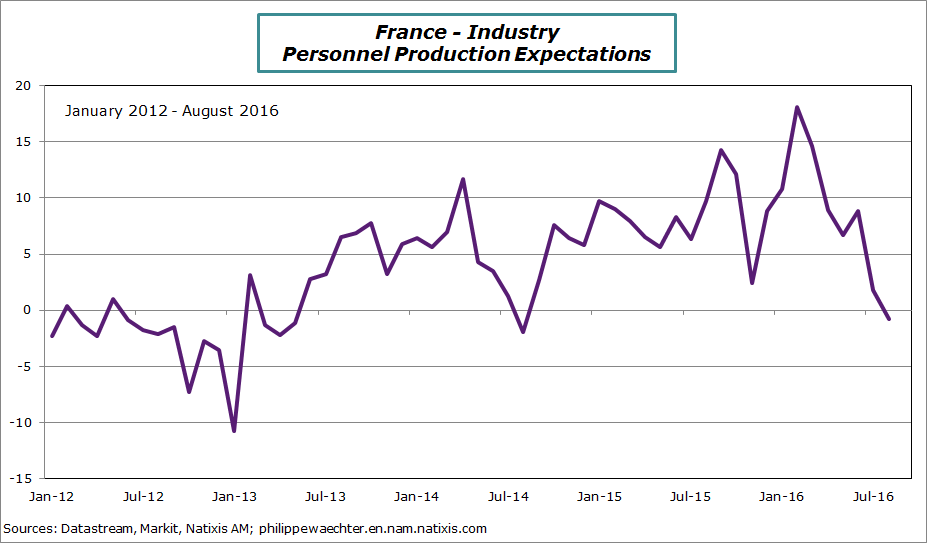

In France, the Personal Outlook index on Production is shifting downward in the industrial sector.

There is, both Germany and France, the perception by companies that the economic activity will not have the necessary impulses that could provoke an acceleration in the economic momentum. This can be linked with Brexit (see here) and its consequences or by the fact that the global situation is at risks and not only on economic side. We see political risks almost everywhere (elections in the US, in France, referendum in Italy, Brexit,…) and this could be a drag for economic growth.

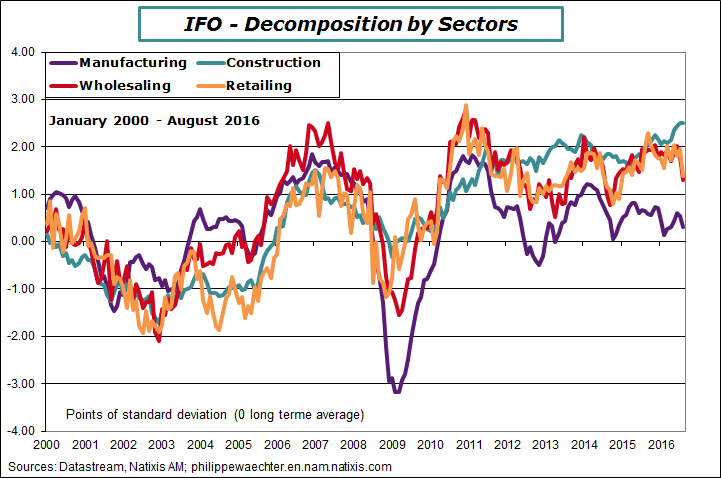

The detail of each survey shows that internal demand has been weaker in August.

This can be seen on the German graph below. There is a deep drop in retailing and in wholesaling in August.

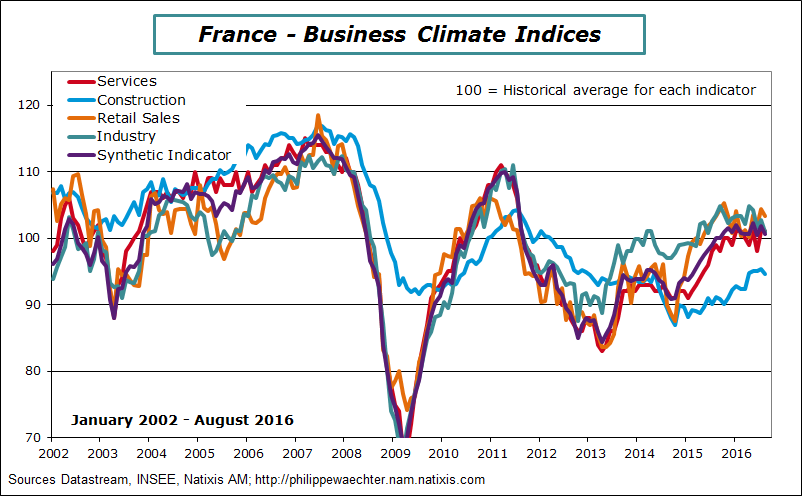

In France the main source of concern is the weaker momentum in the industry. All indices are close to their historical level (except construction) and there is no source of rapid improvement. The industrial sector was perceived as stronger 3 to 6 months ago but this is no longer the case and its recent momentum is problematic. This means that we can have a rebound in the third quarter for GDP (after 0 in Q2) but the government target growth of 1.5% for 2016 will not be reached.