During the second quarter, GDP growth was lower than expected for the Euro Area.

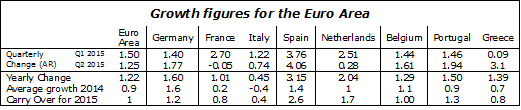

GDP was up by 1.25% (annual rate) after 1.5% during the first three months of the year. Compared to the second quarter of 2014, activity is 1.2% higher. Carry over growth for 2015 is at 1% (average growth for 2015 if GDP level remains at Q2 level during the last two quarters of the year).

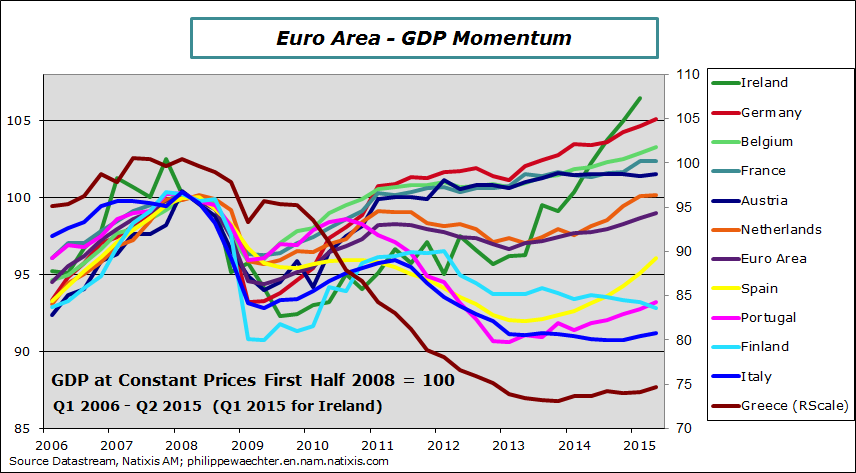

On the graph we see that the trend since the beginning of 2013 remains weak. The recovery after the 2011/2012 recession is not explosive. Since the break after the first quarter of 2011, the average annual growth has just been 0.2%. The recovery since Q1 2013 is just following a 1% trend.

The impact of austerity policies (fiscal and monetary) has been particularly strong in the Euro Area and has a persistent effect.

For 2015, a GDP growth rate at 1.5% is achievable. It will not change ECB monetary policy as there will be no real acceleration. The GDP profile will continue the weak trend seen since the beginning of 2013. Lower oil prices will be a support for consumers expenditures. This will limit the risk of higher inflation. That’s why the ECB will not change its strategy rapidly.

For countries in the Euro Area, figures are as follows on the table (we don’t have details except for France. National institutes made comments on the main drivers of growth but without figures)

For countries in the Euro Area, figures are as follows on the table (we don’t have details except for France. National institutes made comments on the main drivers of growth but without figures)

The strongest country is Spain with a GDP growth rate at 4% in Q2 and a carry over of 2.6%. This performance relies on both external and internal strong momentum.

Germany has accelerated during the second quarter even if it a little less than what was expected. It reflects a strong net exports contribution to GDP growth (mainly exports). Internal demand had a positive contribution on consumption and government expenditures. Investment dynamics was weaker.

In France, there is also a strong performance of net exports but it was compensated with a weaker growth for internal demand (mainly households’ expenditures) and a decrease in inventories. (see a detailed analysis in French here).

In Italy, it is internal demand that was the main driver for growth. Carry-over growth for 2015 is at 0.4%.

The trend is nevertheless positive even if it not that strong as it can be seen on the graph.With the exception of Finland where GDP decreases since 2012, all other countries are on a positive trajectory. Netherlands and France are nevertheless weaker spring.

The trend is nevertheless positive even if it not that strong as it can be seen on the graph.With the exception of Finland where GDP decreases since 2012, all other countries are on a positive trajectory. Netherlands and France are nevertheless weaker spring.

We clearly see the strong performance of Spain and Portugal and of course of Ireland but also of Belgium and Germany. More recently Greece has a had a positive performance (mainly households’ expenditures)