It was initially published in French here

Different elements must be noticed this week to understand the macroeconomic outlook

The first element is Janet Yellen’s speech. She talked one week after the press conference following the last Fed’s monetary committee. In her discussion of the US monetary policy, everyone was able to find what he wanted to find. Pros and cons of a rate hike have arguments in her speech to feed their own perception. The situation remains highly uncertain on monetary policy side

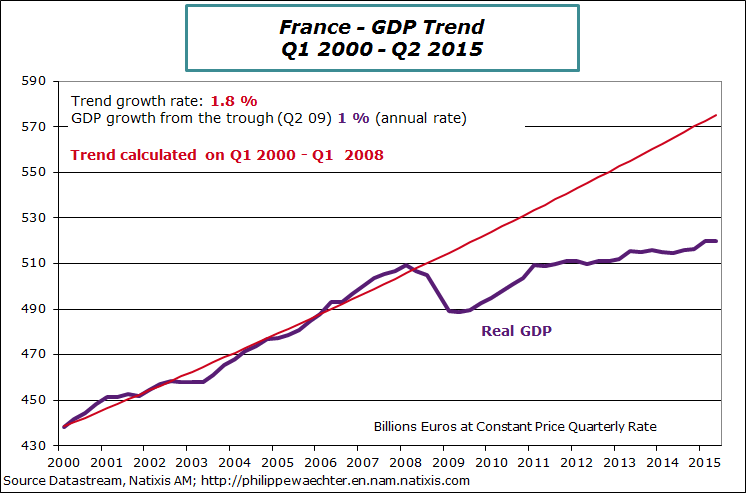

The second point is related to the French economy. With the second GDP estimate for the second quarter, we have details on behaviors. Before that, we note that the French profile is marginally stronger. The first quarter GDP growth is still at 0.7% (non-annualized rate) and the second at 0% but the carry over growth for 2015 is higher at 0.87% versus 0.83%. To converge to 1% which is the government target, a mere 0.18% is needed in each of the two remaining quarters of this year. Before the new estimate it was 0.25%.

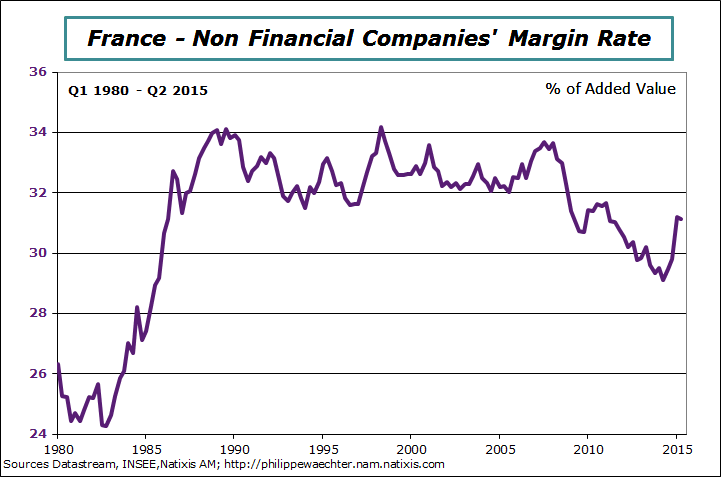

What is important to notice is the impact of the government pro-business strategy. By reducing charges the government has helped companies to improve their margin. It’s not back to the pre-crisis level but margin level is much higher than a year ago. It is also higher than 2014’s average. The current figure is 31.1 versus 29.1 a year ago and 29.5 for 2014. Companies’ financial conditions are currently stronger. The next step is a real acceleration in companies’ investment. This is not currently the case but with the stronger European momentum that is taking place this can be reachable.

What is important to notice is the impact of the government pro-business strategy. By reducing charges the government has helped companies to improve their margin. It’s not back to the pre-crisis level but margin level is much higher than a year ago. It is also higher than 2014’s average. The current figure is 31.1 versus 29.1 a year ago and 29.5 for 2014. Companies’ financial conditions are currently stronger. The next step is a real acceleration in companies’ investment. This is not currently the case but with the stronger European momentum that is taking place this can be reachable.

On this issue we notice that the Business Climate Index follows the same profile than the German IFO. The level is different but profiles are close. The French situation is gaining momentum but still at a low-level. That’s why job seekers number was still increasing in August. The current economic momentum is not sufficient to get a sustainable trend on jobs.

On this issue we notice that the Business Climate Index follows the same profile than the German IFO. The level is different but profiles are close. The French situation is gaining momentum but still at a low-level. That’s why job seekers number was still increasing in August. The current economic momentum is not sufficient to get a sustainable trend on jobs.

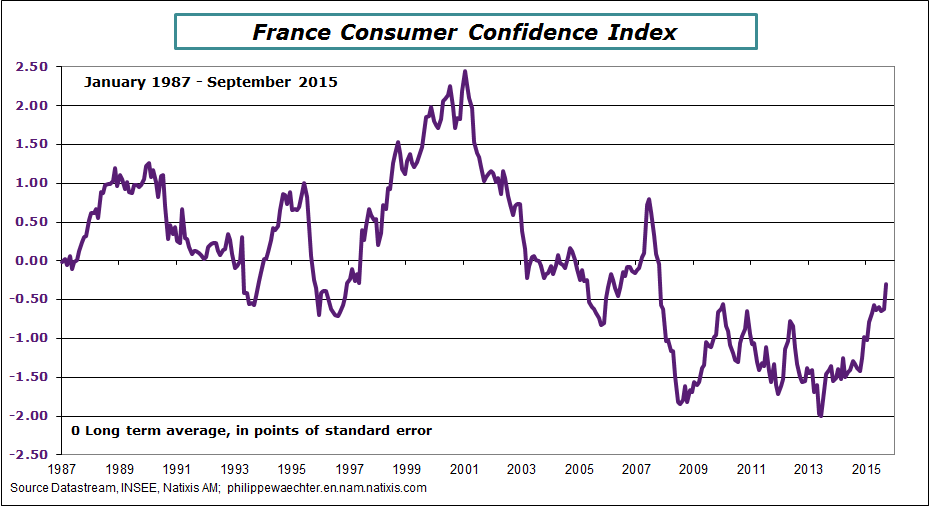

Households’ purchasing power is now stabilized. There was a break in its profile after 2007 and a deep decline after 2012 but now the index is back to 2010/2011 level thanks to the low inflation rate. This improvement must also be associated with the jump in the consumer confidence index. It is, in September, at its highest level since October 2007. Details show a more positive perception of the future.

Households’ purchasing power is now stabilized. There was a break in its profile after 2007 and a deep decline after 2012 but now the index is back to 2010/2011 level thanks to the low inflation rate. This improvement must also be associated with the jump in the consumer confidence index. It is, in September, at its highest level since October 2007. Details show a more positive perception of the future.

That’s an important point for the French economy: both companies and households have a more optimistic perception of the foreseeable future. It means that economic horizon is moving away. Usually this can be associated with a riskier behaviour which is a more favourable environment for growth.

That’s an important point for the French economy: both companies and households have a more optimistic perception of the foreseeable future. It means that economic horizon is moving away. Usually this can be associated with a riskier behaviour which is a more favourable environment for growth.

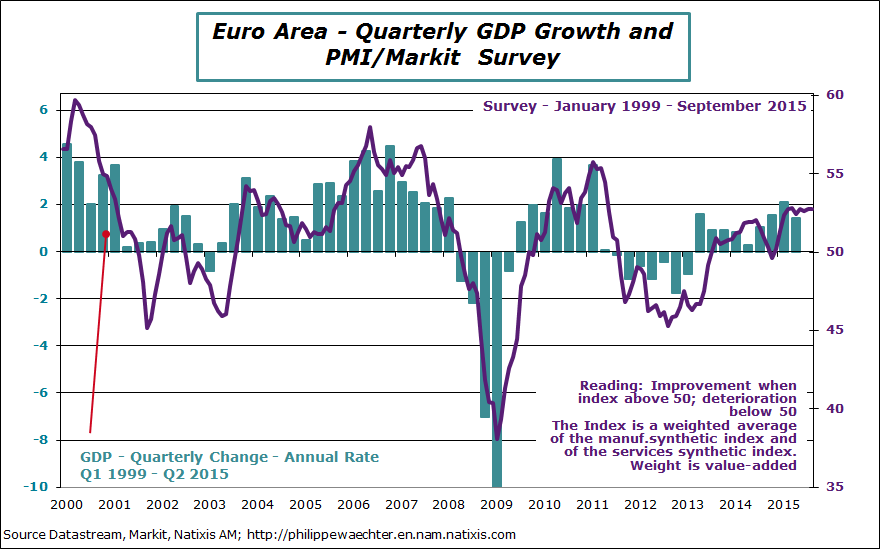

In the Euro Area, the Markit synthetic index for the whole economy is stable in September. Since last February it is at the same level. It reflects positive growth (the index is in a range 52.4 – 52.8) but no acceleration. The target is to have a consistent business cycle within the Euro Area; in that case it would lead to a real acceleration. This is the ECB target but it is not the case yet. The current heterogeneity is a drag for stronger growth.

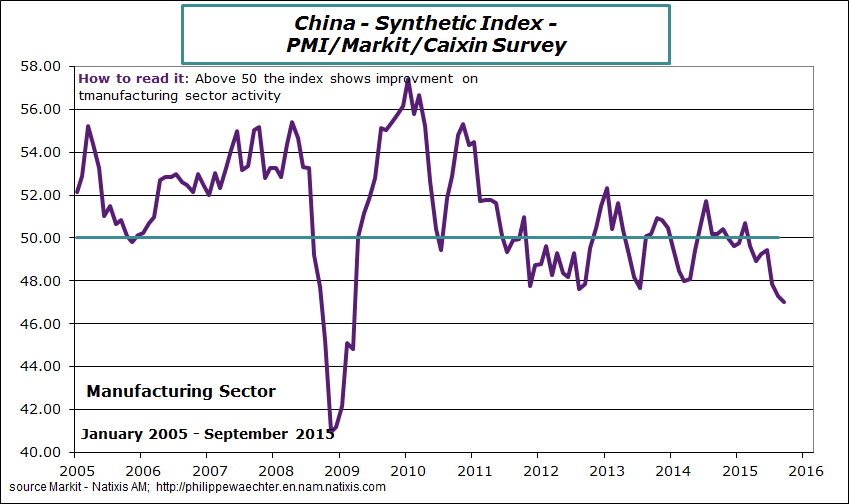

In China, there is still a downward adjustment. The Markit flash estimate for the manufacturing index is lower in September at 47. This is its lowest level since March 2009. New orders momentum is weak and cannot be perceived as a catalyst for a U-Turn of the economic activity. The adjustment is still on the downside.

In China, there is still a downward adjustment. The Markit flash estimate for the manufacturing index is lower in September at 47. This is its lowest level since March 2009. New orders momentum is weak and cannot be perceived as a catalyst for a U-Turn of the economic activity. The adjustment is still on the downside.

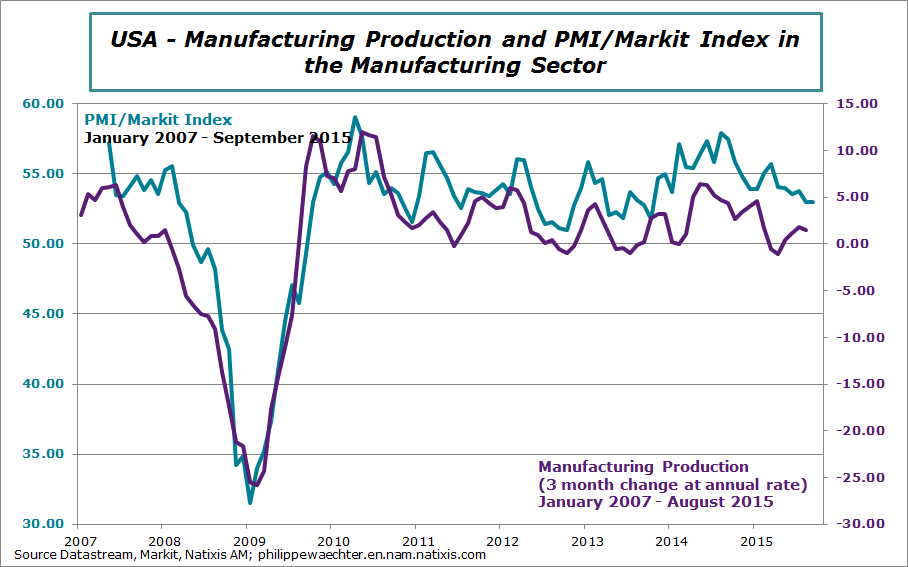

In the USA, the Markit index for the manufacturing sector (flash estimate) is still positive but weaker than what was seen recently. New orders momentum is not as strong as it used to be. This is consistent with a lower dynamics in the manufacturing sector.

In the USA, the Markit index for the manufacturing sector (flash estimate) is still positive but weaker than what was seen recently. New orders momentum is not as strong as it used to be. This is consistent with a lower dynamics in the manufacturing sector.

GDP was revised on the upside for the second quarter. It is now at 3.9% (annual rate) versus 3.7 (previous estimate) GDP growth for the whole year will be above 2.5% and way above the trend observed since the start of the recovery (2.17%). There are no nominal pressures and no immediate incentives for the Fed to act.

GDP was revised on the upside for the second quarter. It is now at 3.9% (annual rate) versus 3.7 (previous estimate) GDP growth for the whole year will be above 2.5% and way above the trend observed since the start of the recovery (2.17%). There are no nominal pressures and no immediate incentives for the Fed to act.

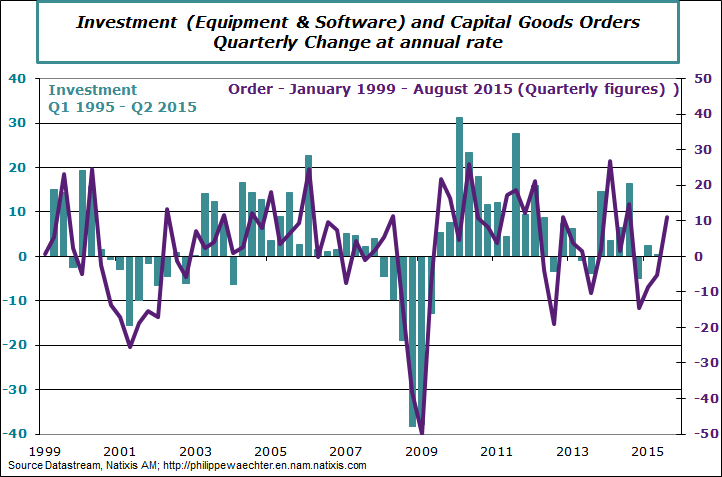

During the third quarter we expect a strong rebound of companies’ investment after the acceleration in capital goods orders in July and August.

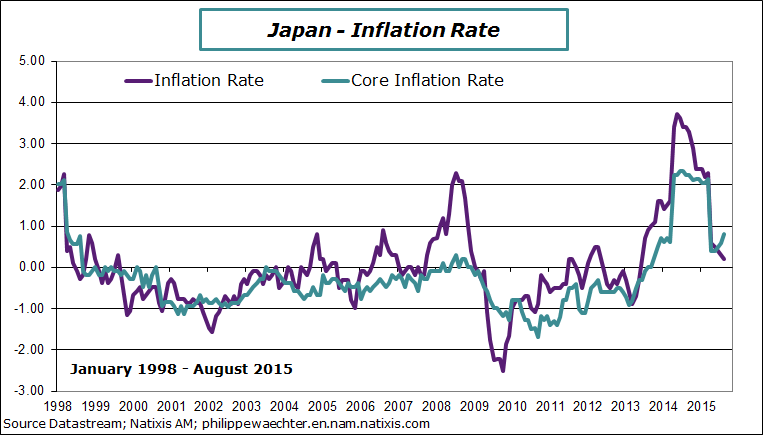

In Japan, the inflation rate is again very low at 0.2% in August. If it follows Tokyo’s index, for which we have September inflation rate, it will be close to zero in September. The core inflation rate is at 0.8%.

In Japan, the inflation rate is again very low at 0.2% in August. If it follows Tokyo’s index, for which we have September inflation rate, it will be close to zero in September. The core inflation rate is at 0.8%.

Shinzo Abe has buried the Abenomics. The new targets on growth, social security and family policy lack of consistency (I will come back later on this issue)

Shinzo Abe has buried the Abenomics. The new targets on growth, social security and family policy lack of consistency (I will come back later on this issue)

For the week to come, the main publication will be the ISM and Markit surveys for the manufacturing sector (Thursday) and the employment report in the USA (Friday). On Wednesday, inflation for September in the Euro Area will be release. The number will probably be negative.